By: Connor Mycroft

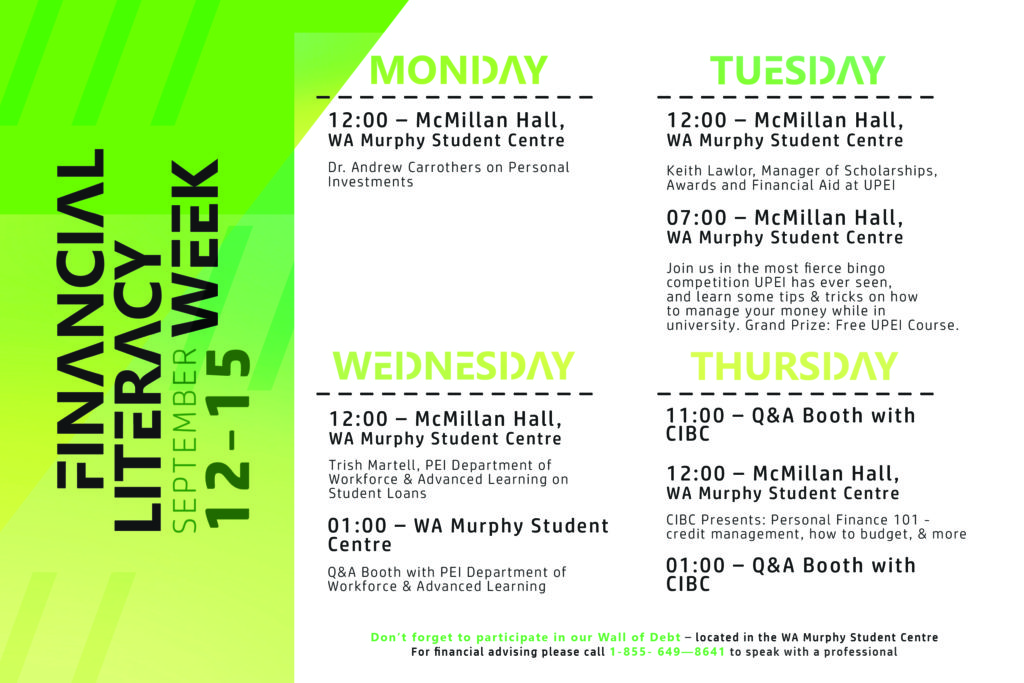

There I was, sitting in a mostly-vacant McMillan Hall, waiting for Trish Martell from the Department of Workforce & Advance Learning to begin her presentation on student loans as a part of Financial Literacy Week.

Surely more students will be arriving soon, I thought to myself. There must be more than this baker’s dozen interested in learning about that money that somehow appears in their account each semester. Every time I check social media it seems I stumble across somebody complaining about rising tuition costs, sharing a video advocating “free†university, or otherwise putting their financial woes on open display. I imagine that’s what the other students attending were doing, because instead of listening to the presentation they had their headphones in and their eyes glued to their computer screens. Where are all those highly engaged, concerned students I hear about all the time?

For many, student loans are a lifeline. Without them, how else would they be able to pay for their education and still go to that music festival they traveled halfway across the country for over the summer? How else would they be able to afford their weekly bender that allows them to forget all that stuff they learned that week? How else would they be able to flaunt their government-provided cash to impress that girl (or boy) they’ve been eyeing from across the lecture theater all week?

Perhaps I’m being too disparaging with that last paragraph, but I bet I got a reaction out of you.

Because I know what it’s like to finally be put in charge of paying for your own education, and not knowing how the hell you are going to do it. Because I know the juggling act that is balancing a full course load while working a demanding job, and why you may have chosen to ditch the latter. Because I know what it’s like to have a maxed out credit card and be reduced to scrounging for change to buy instant ramen. Because I know what it’s like to come from a lower-income family that can hardly support themselves, let alone your studies. Because I know what it’s like to start the new year only to find out that tuition costs have risen again. Because I realize how necessary student loans are, and because I am very aware of how little I knew about them when I got my first one.

Which is why I was so disheartened to see so few students, and how pleased I was when the opening line of the presentation was “typically student loan payments are the last thing on people’s minds.â€

Case in point.

I could just end this article here. If you weren’t interested enough to attend this heavily advertised event, why would you be interested in reading the regurgitation of it here? Why should I go through the hassle? I mean, how many of you have actually made it this far into the article anyways? However, I realize that it’s still the first real week of classes, and there are plenty of other things to worry about than an unneeded presentation. I’m sure many of you were in class, and no doubt many of you have probably just used yours student loans to pay for tuition. So, out of the kindness of my heart, I will provide you a brief recap.

Did you know that there can be both a federal and provincial portion to your student loan, depending on how much you choose to borrow? A Canada Student Loan will cover you for the first $7,140 you borrow each year, which typically goes to covering first semester costs. Repayment starts 6 months after your end date of studying, at a current interest rate of 5.2%. So does that mean you can just wait until 6 months later to begin repaying? Yes, but you may want to start earlier, as that interest begins accumulating the day after you end your studies.

If you are required to borrow more than the federal portion allows, you will apply for a Provincial Student Loan. Islanders can receive up to $5,950 per year, and payments don’t begin until 1 year after your end of study. On top of that, the provincial portion of your loan has a 0% interest rate, so long as you keep in good standing. I’ll return to this in a moment.

So how much might you owe in the end, and how long will it take you to repay it? Hypothetically speaking, if you are required to borrow the maximum each year, both federally and provincially, you will end up owing a staggering $40,000. Your total monthly student loan payment will be $460.69, which you will be repaying for 9 1/2 years! How’s that second job looking?

Once the six month grace period is up and your repayment begins, it’s important to remember that the payments begin being deducted automatically from the same account in which your loan funds were deposited. Although a representative will contact you before the first payment, if you have changed your address or phone number without updating your account you may be in for a surprise when your rent money suddenly disappears. Also, Student Loans are the same as any other kind of loan, and failing to pay will have grave consequences on your credit score. This means you may not be approved for that car you’ve always wanted, forcing you to continue driving to work in your parent’s hand-me-down beater.

If you know you are going to have troubles making payments, it is imperative that you contact your loan providers before you get behind. If you wait until after, your options become severely limited. If you are quick to inform them, you may be able to have repayments placed on hold for up to 6 months. You may also be eligible for the Debt Reduction Grant, shaving off up to $2,000 per year of study. To be eligible, you must have borrowed a minimum of $6,000 federally and $100 provincially. Keep in mind, you only have 1 year after graduating to apply. Also, beginning later this year, graduates earning less than $25,000 will not be required to make Canada Student Loan payments until they reach that income threshold. Thanks Trudeau!

If you do find yourself in the unfortunate circumstances of defaulting on your Provincial Student Loan, which happens once you are in arrears for 270 days, you’ll probably end up homeless.

No, it isn’t that bad, but it can be pretty miserable. And you could wind up being homeless, or at least moving back in with your parents, if you haven’t already.

For one, remember that lovely 0% interest rate I told you about? Well that’s going to increase to the rate of prime + 2%, which today would mean 4.7%. You’ll also be registered with the CRA’s set-off program, so while they provide amnesty to millionaire tax-evaders with offshore accounts (real thing by the way, look it up), they are going to claw back your HST Credits and your yearly Tax Refund (which basically disappears once you’re done being a student anyways. Just a heads up.) It can also make you ineligible for any further student loans or grants, so if you are an Arts student coming to the realization that the only way to get a decent paying job in your field is to spend a further 2-4 years in school, you may want to take note.

All is not lost, however, if you do default. The province provides a Rehabilitation Program for all you spending junkies out there which allows you to reverse some of those consequences. All it requires is that you make payments to their office for 6 months. You were good at that before, right?

I would like to mention that when the presentation concluded, McMillan Hall burst out into thunderous applause, complements of two people sitting at the front. The scheduled Q&A session did not take place, or at least, not in the same forum it was intended for. The projector was shut off. And then McMillan Hall filled up with students.